Key Highlights

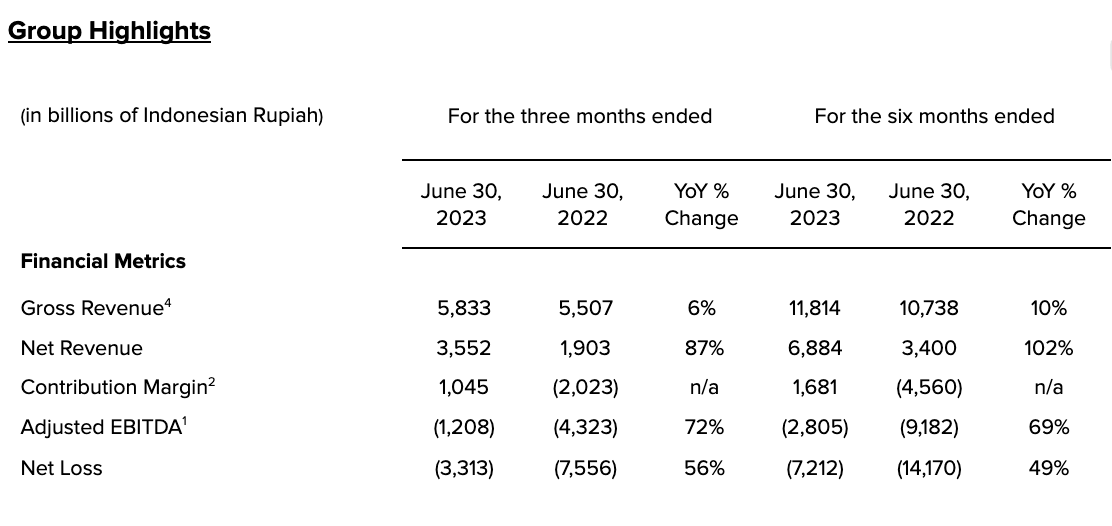

- Group Adjusted EBITDA1 improved by 72% year-on-year (YoY) to Rp -1.2 trillion — the sixth consecutive quarter of improvement

- Group contribution margin2 expanded to 0.73% of GTV3, increasing 207 basis points (bps) YoY and 30 bps quarter-on-quarter (QoQ) to Rp 1.0 trillion

- Gross revenue4 improved by 6% YoY to Rp 5.8 trillion

- Incentives and product marketing decreased by 43% YoY, reflecting savings of Rp 2.7 trillion for the quarter

Jakarta, Indonesia, August 15, 2023 – PT GoTo Gojek Tokopedia Tbk (IDX: GOTO, “GoTo Group” or the “Company”), the largest digital ecosystem in Indonesia, today announced its second quarter 2023 financial results*, reporting Adjusted EBITDA1 improvement of 72% YoY to Rp -1.2 trillion, driven by improved monetization and ongoing incentive optimization.

Patrick Walujo, GoTo Group CEO, said: “Our commitment to reaching positive Adjusted EBITDA1 this year remains on course, however, breaking even is not the end goal - we must go on to deliver sustainable and profitable growth. This will require sharper execution with the utmost urgency as well as increasing our total addressable market. Having built a strong presence among the convenience consumers, we intend to expand our consumer base, without the use of unsustainable incentives, among budget consumers who prioritize value for money. We are developing a long-term strategy for achieving this, and in the meantime we will continue to operate with absolute cost discipline as we pivot our product mix towards the mass market.”

Jacky Lo, GoTo Group CFO, said: “We have progressed against our key profitability metrics for the sixth consecutive quarter as we further dialed-back unproductive incentive and product marketing programs, while maintaining our focus on profitable users. Revenues were up year-on-year as a result of growing monetization across our businesses, with our Group take rate reaching 4.1% - a year-on-year increase of 40 bps. We continued to maintain tight cost discipline and reaffirm our guidance to reach positive Adjusted EBITDA1 within Q4 of this year. Due to our better than expected progress, we are revising our full year 2023 Group Adjusted EBITDA1 guidance to between Rp -4.5 and Rp -3.8 trillion.”

In the second quarter of 2023, the Company further optimized monetization and reduced costs throughout the organization. Gross revenue4 increased 6% YoY to Rp 5.8 trillion amid continued incentive and product marketing cost reductions of 43% YoY, resulting in savings of Rp 2.7 trillion for the quarter. Group contribution margin2 remained positive for the second consecutive quarter at 0.73% of GTV3, increasing 207 bps YoY and 30 bps QoQ to reach Rp 1.0 trillion.

GoTo’s cash position and balance sheet remain solid. With Rp 25.4 trillion of cash and cash equivalents and a credit facility of approximately Rp 4.65 trillion, of which Rp 3.1 trillion was undrawn as of June 30, 2023. The Company remains confident that it will reach positive operating cash flow without any additional external funding.

2Q23 Group Adjusted EBITDA1 was Rp -1.2 trillion, or -0.84% of GTV3, improving by 72% YoY.

GoTo Group maintained positive YoY gross revenue4 growth of 6% as a result of growing monetization across GoTo’s ecosystem, as the overall take rate for the Group increased by 40 bps YoY to 4.1%.

Group GTV3 for the quarter was Rp 143.7 trillion, a slight decrease of 5% YoY, mainly as a result of reduced incentives and product marketing, but also driven by seasonal factors such as the higher number of public holidays in Indonesia in April and June.

In 2Q23, the number of profitable users and overall profitability per user remained stable QoQ, with profitable users contributing close to 75% of total GTV3. User engagement continued to improve, as shown by the increase in spending per user of 42% YoY.

Net Loss narrowed by 15% QoQ and 56% YoY to Rp 3.3 trillion, driven by healthy revenues and reduced incentives and product marketing spend, which dropped by 43% YoY, reflecting quarterly savings of Rp 2.7 trillion.

Economy-focused products and Gojek’s multimodal product, the first of its kind in the region, continued to generate new users while successfully reactivating dormant users, in line with On-demand Services’ core growth strategy to expand its Total Addressable Market (TAM) by catering to budget consumers.

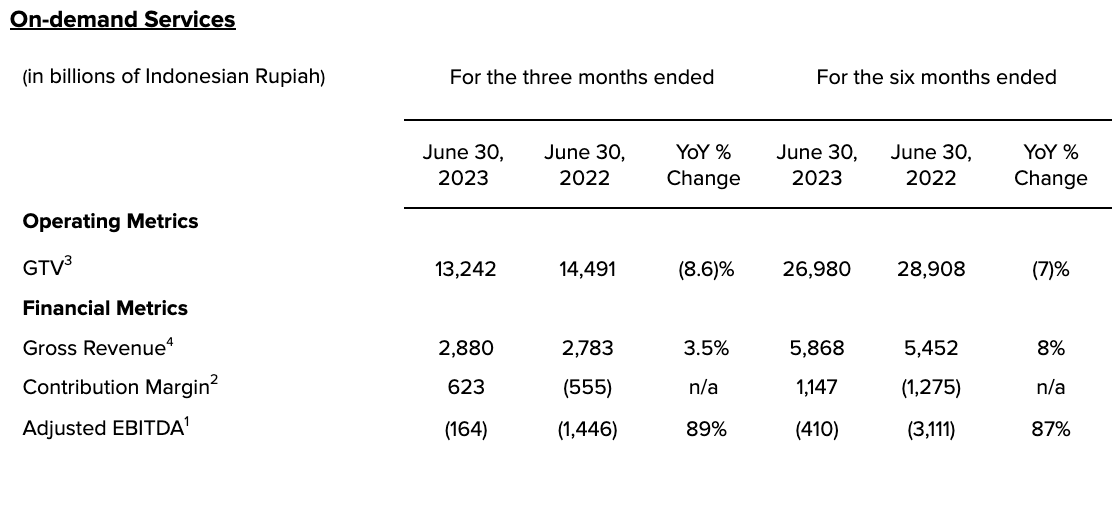

- Adjusted EBITDA1 for On-demand Services improved by 89% YoY, to -1.24% of On-demand Services GTV3.

- Gross revenue4 continued to grow at a steady pace, increasing by 3.5% YoY in the second quarter to Rp 2.9 trillion, as a result of the Company’s ongoing focus on profitability and monetization.

- Incentives and product marketing expenses decreased by 35% YoY, equivalent to Rp 1 trillion in savings for the quarter.

- Lower costs and increased monetization drove a positive contribution margin2 for On-demand Services for the third consecutive quarter, reaching 4.7% of GTV3, up by 853 bps YoY.

- On Demand Services GTV3 declined to Rp 13.2 trillion, a decrease of 8.6% YoY as the Company rationalized incentives to focus on profitable users. This was also exacerbated by a higher number of public holidays in Indonesia, which primarily impacted Transport and Food.

- The Company’s analysis shows that the market potential of On-Demand Services can double if it expands its reach to fully accommodate Budget Consumers. It will therefore focus on addressing this segment through products that offer additional appeal, flexibility and quality - specifically GoFood Hemat, GoCar Hemat and GoTransit Multimodal.

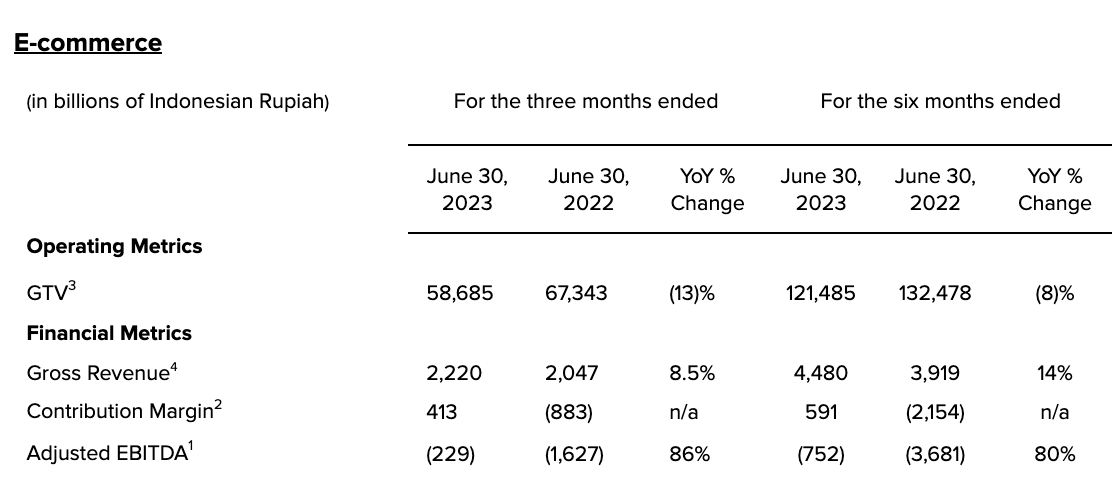

In the E-commerce segment, strong progress has been made in monetization as commission adjustments implemented earlier in the year have taken effect. Throughout the first half of 2023, experimentation has taken place with GTL’s in-house logistics capabilities. Results have been very promising, with GTL enabling a 15% reduction in overall E-commerce logistics' costs. This will improve further as penetration of GTL on Tokopedia grows.

- Adjusted EBITDA1 for E-commerce improved by 86% YoY, to -0.39% of E-commerce GTV3.

- E-commerce contribution margin2 remained positive for the second consecutive quarter in 2Q23, improving sequentially to 0.7% of GTV3 and increasing by 201 bps YoY.

- Bottom-line improvement in E-commerce was attributable to the rationalization of incentives and product marketing spend by 48% YoY, equivalent to Rp 1.2 trillion of savings for the quarter.

- E-commerce GTV3 declined to Rp 58.7 trillion, down 13% YoY, primarily due to a reduced number of transactions from low-quality users owing to decreased blanket incentives. Seasonal factors such as the increased number of public holidays also drove this decline, as did the winding down of parts of the Mitra Tokopedia business announced in March. Excluding Mitra Tokopedia, the GTV3 decline would have been 10% rather than 13%.

- Overall monetization in E-commerce improved as indicated by growth in E-commerce gross revenue4 to Rp 2.2 trillion, an increase of 8.5% YoY.

- Merchants remain loyal to GoTo’s platform, despite increased commissions imposed earlier in the year, bearing testament to the value GoTo’s unique ecosystem provides for merchants and users such as GoPayLater and GoTo’s cash loan product that is now available in Tokopedia.

- In addition to adding more cross-over payment products to E-Commerce, the Company is improving its personalized discovery through engaging content, as well as supporting merchant partners to make their advertising more powerful and engaging using new formats that cater to budget consumers.

- Ongoing collaboration with GoTo Logistics will enable further reductions in overall logistics costs and more efficient shipping subsidies over the coming quarters.

The recent launch of the GoPay app will enable GoTo to amass a broader and more inclusive user base beyond the Gojek and Tokopedia platforms, ultimately also serving as an effective tool for rolling out financial services to new users. GoTo’s cash loan product has also become more accessible with its recent launch on Tokopedia.

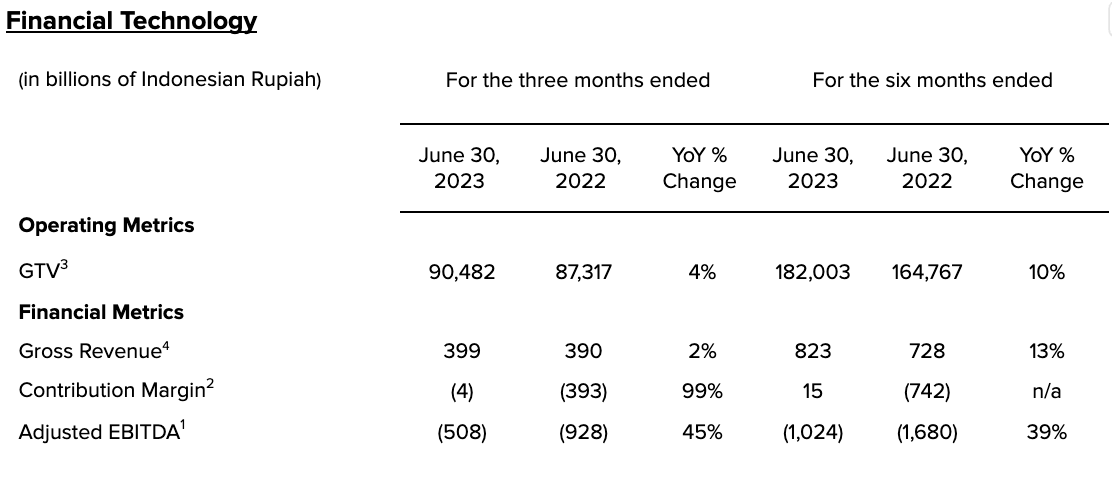

- Adjusted EBITDA1 for Financial Technology improved by 45%, to -0.56% of Financial Technology GTV3.

- Gross revenue4 for Financial Technology increased 2% YoY to Rp 399 billion in 2Q23.

- Financial Technology contribution margin2 improved 45 bps YoY to approximately breakeven. Fluctuations in contribution margin2 are expected in future periods as the Company continues to invest in this space and introduce new products that build out its suite of offerings.

- Spending efficiency within the Financial Technology segment continues to improve while the business grows sustainably as a result of efforts to expand use cases for GoPay users. Incentives and product marketing spend improved by 59% YoY, equivalent to Rp 367 billion in savings for the quarter.

- Financial Technology GTV3 was Rp 90.5 trillion in the second quarter, increasing 4% YoY.

- More rapid product rollouts, particularly in consumer lending, are expected to drive growth in Financial Technology and, in turn, prompt additional consumer spending across the GoTo ecosystem. The recent launches of cash loan products on Tokopedia and the GoPay app will support more open-loop lending adoption and are expected to increase the cash loan book.

- Outstanding loans generated from GoTo’s consumer lending business grew by 21% QoQ to Rp 1.0 trillion as of 2Q23. The Company will continue to scale its loan book origination in 2023 in close collaboration with Bank Jago, while maintaining a competitive lending portfolio, achieved through effective credit risk management.

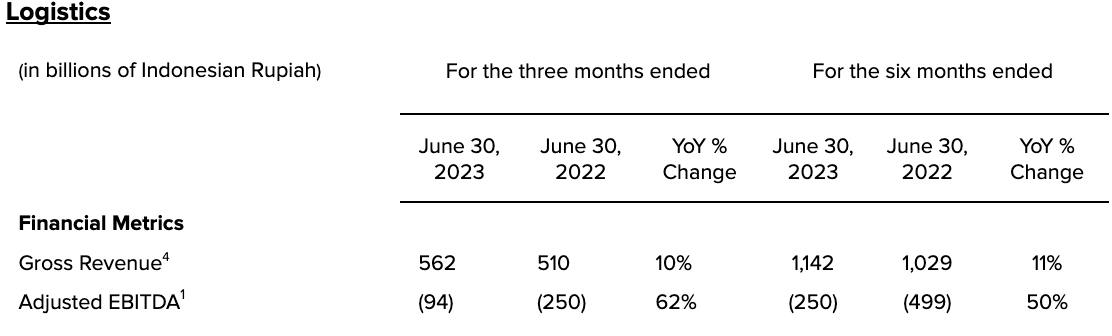

The combination of Tokopedia’s fulfillment unit and Gojek’s E-commerce same-day delivery unit under GoTo Logistics has made processes more efficient on a cross-platform basis. Under this formation, GoTo Logistics has reduced the cost of deliveries for buyers and merchants and enhanced the efficiency of shipping subsidies, while growing its revenues and Adjusted EBITDA1.

- Adjusted EBITDA1 was Rp -94 billion, an improvement of 62% YoY.

- 2Q23 gross revenue4 for GoTo Logistics was Rp 562 billion, a 10% increase YoY.

- Cost structure improvements included reduced incentives and marketing spend by 64% YoY, equivalent to Rp 122 billion in savings for the quarter.

- GoTo Logistics currently supports around one-fifth of Tokopedia deliveries. Increasing this penetration will further drive down logistics costs. Shipping subsidy cost per order has been reduced by around 15% year to date.

- Looking ahead, GoTo Logistics seeks to further reduce consumers’ logistics costs by scaling up its in-house delivery service and fulfillment capacity and leveraging its in-house allocation engine to direct orders to the most efficient third-parties, where applicable.

Environmental, Social and Governance (ESG)

GoTo continues to make operational shifts across its business, ensuring that it is in line with global and industry best practices when it comes to ESG performance. Outcomes from the Company’s efforts in 2Q23 include:

- Electrum, a joint venture between GoTo and TBS Energi Utama, commenced construction of a two-wheel electric vehicle (EV) factory, which will enable local manufacturing of EVs and related components.

- Achieved nine million kilometers on two-wheel EVs under the GoRide Electric limited trial.

- Publication of a study by the University of Indonesia’s Institute for Economic and Social Research – Faculty of Economics and Business (LPEM FEB UI) on the positive effects that the GoTo ecosystem has on its partners. Approximately 91% of GoTo’s business partners use financial services, above the national average.

- The study also showed that the GoTo ecosystem enhances gender equality, with merchants and sellers in the GoTo ecosystem employing two or three workers on average, with more than 50% of these employees being female.

- GoTo's most recent ESG report was awarded a gold-standard Asia Sustainability Reporting Rating (ASRRAT) for the third consecutive year.

Company Outlook

GoTo expects to capture additional growth in broad user demographics in a more cost effective manner across the expansive Indonesian market by leveraging its unique ecosystem that spans the full range of consumer spending.

The Company currently expects:

- To achieve positive Group Adjusted EBITDA1 within the fourth quarter of 2023.

- Full year 2023 Group Adjusted EBITDA1 to be between Rp -4.5 and Rp -3.8 trillion. This is revised from the previously expected range of Rp -5.3 and -4.6 trillion, owing to the significant progress made in the first half.

The above outlook is based on current market conditions and reflects the Company’s preliminary estimates, which are all subject to various uncertainties, including those related to cost inflation and the COVID-19 pandemic.

-END-

About GoTo Group

PT GoTo Gojek Tokopedia Tbk (GoTo Group) is the largest digital ecosystem in Indonesia. GoTo’s mission is to “empower progress” by offering technology infrastructure and solutions that help everyone to access and thrive in the digital economy. The GoTo ecosystem consists of On-demand Services (mobility, food delivery, and logistics), E-commerce (third party marketplaces + official stores, instant commerce, interactive commerce, and rural commerce), and Financial Technology (payments, financial services, and technology solutions for merchants) through the Gojek, Tokopedia, and GoTo Financial platforms.

Forward-Looking Statements

This document may contain forward-looking information or forward-looking statements (collectively, “forward-looking information”). All information contained in this document that is not clearly historical in nature or that necessarily depends on future or subsequent events is forward-looking information prepared as of the date of this document is based upon the opinions and estimates of management as well as the information available to management as of the date of this document. In some cases, forward-looking information can be identified by the use of forward-looking terminology such as "expect", "likely", "may", "will", "should", "intend", "anticipate", "potential", "proposed", "estimate" and other similar words, expressions and phrases, including negative and grammatical variations thereof, or statements that certain events or conditions "may,” or "will" happen, or by discussion of strategy.

Forward-looking information is based upon a number of current internal expectations, estimates, projections, assumptions and beliefs that, while considered reasonable by management, are inherently subject to significant business, economic, competitive and other uncertainties and contingencies. Forward-looking information is not a guarantee of future performance and involves known and unknown risks, uncertainties and other factors (including the risks and uncertainties in the Company’s consolidated financial statements and Management’s Discussion & Analysis available on the Company’s website), that may cause actual results, performance or achievements to be materially different from the future results, performance or achievements expressed or implied by such forward-looking information. Any estimates, investment strategies or views expressed in this document are based upon current market conditions, and/or data and information provided by unaffiliated third parties, and are subject to change without notice. To the extent any information in this document was obtained from third party sources, the Company has not independently verified that information, and there is a risk that the assumptions made and conclusions drawn by the Company based on such information are not accurate. Except as required by law, the Company disclaims any obligation to update or revise any forward-looking information, whether as a result of new information, events or otherwise. Readers are cautioned not to put undue reliance on this forward-looking information and should not be viewed, in and of itself, as any basis for making any investment decision.

Non-IFAS Financial Measures

GoTo Group uses the following non-Indonesian Financial Accounting Standards (IFAS) financial measures including gross revenue4, contribution margin2 and Adjusted EBITDA1, to understand and evaluate GoTo Group’s core operating performance. However, the definitions of GoTo Group’s non-IFAS financial measures may be different from those used by other companies, and therefore, may not be comparable. Furthermore, these non-IFAS financial measures have certain limitations in that they do not include the impact of certain expenses that are reflected in GoTo Group’s consolidated financial statements that are necessary to run GoTo Group’s business. Thus, these non-IFAS financial measures should be considered in addition to, not as substitutes for, or in isolation from, measures prepared in accordance with IFAS.

Non-IFAS measurements are not intended to replace the presentation of GoTo Group’s financial results in accordance with IFAS. Rather, GoTo Group believes that the presentation of Adjusted EBITDA1 provides additional information to investors to facilitate the comparison of past and present results, excluding those items that GoTo Group does not believe are indicative of GoTo Group’s ongoing operations due to their size and/or nature. In addition, GoTo Group also presents Contribution margin2, which may provide additional information to investors in relation to the results excluding non-variable expenses and other income/expenses. Contribution margin2 and Adjusted EBITDA1 presented herein may not be comparable to similarly entitled measures presented by other companies, who may use and define these measures differently. Accordingly, you should not compare these non-IFAS measures to those presented by other companies.

Unaudited Consolidated Financial Information

GoTo Group furnished the results for the six months ended June 30, 2023 and 2022. The information for the six months ended June 30, 2023 is extracted from the consolidated financial statements of the Company as of and for the six months ended June 30, 2023 (with consolidated financial information for the six months ended June 30, 2022, that has not been reviewed and not been audited, disclosed as comparative) that has been reviewed in accordance with Standard on Review Engagements 2410, “Review of Interim Financial Information Performed by the Independent Auditor of the Entity”, established by the Indonesian Institute of Certified Public Accountants. The information pertaining to the consolidated financial information for the six months ended June 30, 2022 that is presented in this document has not been audited, reviewed, examined, or applied any procedures on. Accordingly, there are no opinions or any other form of assurance expressed with respect to the period of six months ended June 30, 2022.

Furthermore, in this document, GoTo group also furnished the results of the three months ended June 30, 2023, March 31, 2023 and June 30, 2022 which have been prepared by and are the responsibility of management. The consolidated financial information for the three months ended June 30, 2023, March 31, 2023 and June 30, 2022 have not been audited, reviewed, examined, or applied any procedures on. Accordingly, there are no opinions or any other form of assurance expressed with respect to any and all consolidated financial information for the three months ended June 30, 2023, March 31, 2023 and June 30, 2022 presented in this document.

* The Company has published its consolidated financial statements as of and for the six months ended June 30, 2023, which have undergone limited review by an independent auditor.

1 GoTo Group calculates the Adjusted EBITDA, a non-IFAS financial measure, beginning with loss before income tax and adjusting for (i) depreciation and amortization expenses; (ii) finance income; (iii) interest expenses; (iv) loss on impairment of assets of disposal group classified as held for sale; (v) (reversal)/loss on impairment of investment in associates and joint ventures; (vi) loss on impairment of goodwill; (vii) fair value adjustment of financial instruments; (viii) loss on impairment of intangible and fixed assets; (ix) share-based compensation cost (including for the Gotong Royong Program); (x) unrealized foreign exchange (gain)/loss from cash remeasurement; (xi) share of net losses in associates and joint ventures; (xii) (gain)/loss on divestment and dilution of investment in associates and joint ventures, net (xiii) dividend income; and (xiv) non-recurring items.

2 GoTo Group calculates the contribution margin, a non-IFAS measure, beginning with net revenue and deducting total cost of revenues, a portion of sales and marketing expenses relating to the promotional excess and product marketing and others consists of mainly withholding taxes related to sales and marketing expense and other insignificant expenses.

3 GTV means gross transaction value, an operating measure representing:

a. the sum of the time value of the transactions from On-demand Service.

b. the sum of the value of the product and services recorded on our E-commerce Segment.

c. the sum of the total payments volume, or TPV processed through our platform of Financial Technology Services.

d. and excluding amounts from inter-Company transactions between entities within the Company that are eliminated upon consolidation.

4 Gross revenue represents the total Rupiah value attributable to GoTo Group from each transaction, without any adjustments for incentives paid to driver-partners and merchant partners or promotions to end-users, over the period of measurement. For a reconciliation of net revenue to gross revenue, please refer to the section “Non-IFAS Financial Reconciliation.”

Contacts:

Media

GoTo Group: corporate.affairs@gotocompany.com

Investors/analysts

GoTo Group: ir@gotocompany.com

The Piacente Group: goto@thepiacentegroup.com