Key Highlights

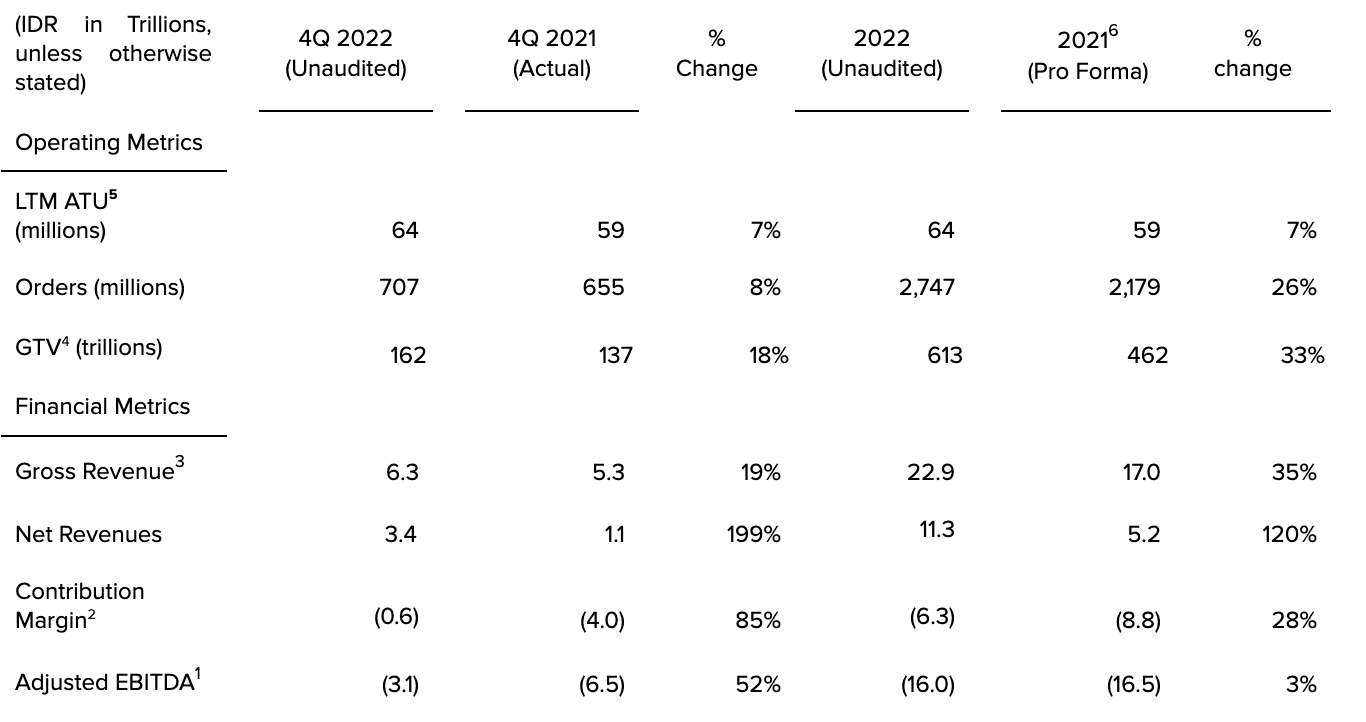

- 4Q22 adjusted EBITDA1 improved by 52% YoY and 15% QoQ to Rp -3.1 trillion - the fourth consecutive quarter of improvement

- 4Q22 Group contribution margin2 improved by 85% YoY and 51% QoQ, exceeding guidance

- 4Q22 Gross revenue3 up 19% YoY to Rp 6.3 trillion, in line with guidance

- Reduced incentives and product marketing in 4Q22 by 34% YoY, or Rp 2.8 trillion, with - further reductions through extensive management of fixed costs

- Information presented solely as indicative position and results based on unaudited consolidated selected financial information as of and for the year ended December 31, 2022 - audited consolidated financial statements as of and for the year ended December 31, 2022 are scheduled for publication by end of March 2023.

Jakarta, Indonesia, March 20, 2023 – PT GoTo Gojek Tokopedia Tbk (IDX: GOTO, “GoTo Group” or the “Company”), the largest digital ecosystem in Indonesia, today announced indicative full year and fourth quarter 2022 financial results, which saw Adjusted EBITDA1 improve by 52% year-over-year (YoY) to Rp -3.1 trillion in 4Q22, marking four consecutive quarters of improvement, driven by a solid performance from the On-demand Services segment. Gross revenue3 grew 19% YoY to Rp 6.3 trillion over the same period.

Andre Soelistyo, GoTo Group CEO, said: “We have made considerable progress on our accelerated path to profitability, with particularly strong results in the fourth quarter. The scaling back of incentives and product marketing spend has not come at the expense of revenue growth, thanks to a sharpened focus on key monetization drivers that target high-quality, profitable users. This, along with a disciplined approach to costs, is powering our profitability push. Although we expect growth to moderate in the short term, we will continue to focus on building the foundational product infrastructure that will drive sustainable, profitable growth over the long term. As we look ahead, the first two months of 2023 show even faster progress*, meaning we are on track to reach positive adjusted EBITDA1 within the fourth quarter of 2023.”

The Group continued to advance its cost optimization strategy across the business during the quarter. Growth in monetization, coupled with rationalization in incentives and promotional spending, resulted in fourth quarter Group contribution margin2 improving YoY by 254 basis points to reach -0.4% of total GTV4, which also grew by 18% YoY to Rp 162 trillion. Notably, the On-demand Services segment became contribution margin2 positive for 4Q22, a full quarter ahead of guidance.

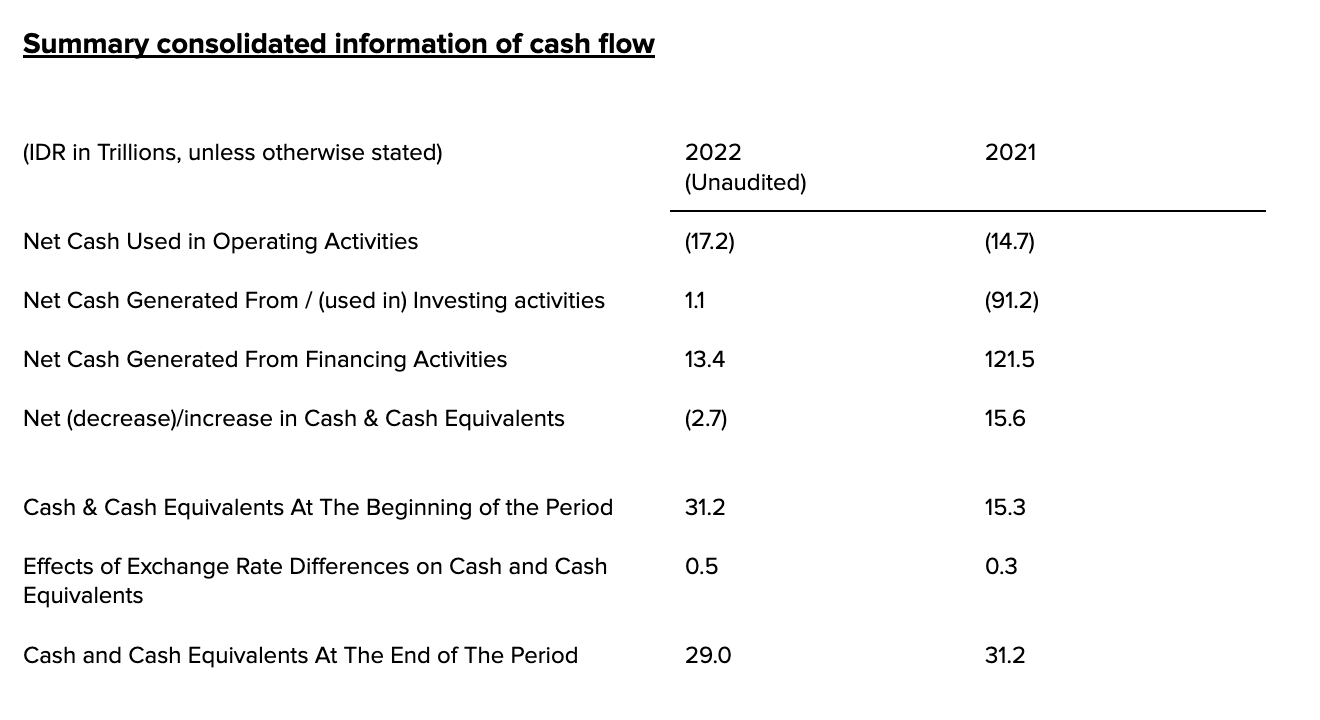

Jacky Lo, GoTo Group CFO, said: “Throughout 2022, growth was resilient in spite of macroeconomic headwinds, while we continued to manage our costs by embedding structural efficiencies throughout the Company. Our goal is to drive cost savings and expense reductions, which have already yielded faster than expected profitability improvements. We are very encouraged by the results to date and our confidence is underpinned by our solid cash position, which is sufficient to allow us to reach positive operating cash flow as we near our profitability targets this year.”

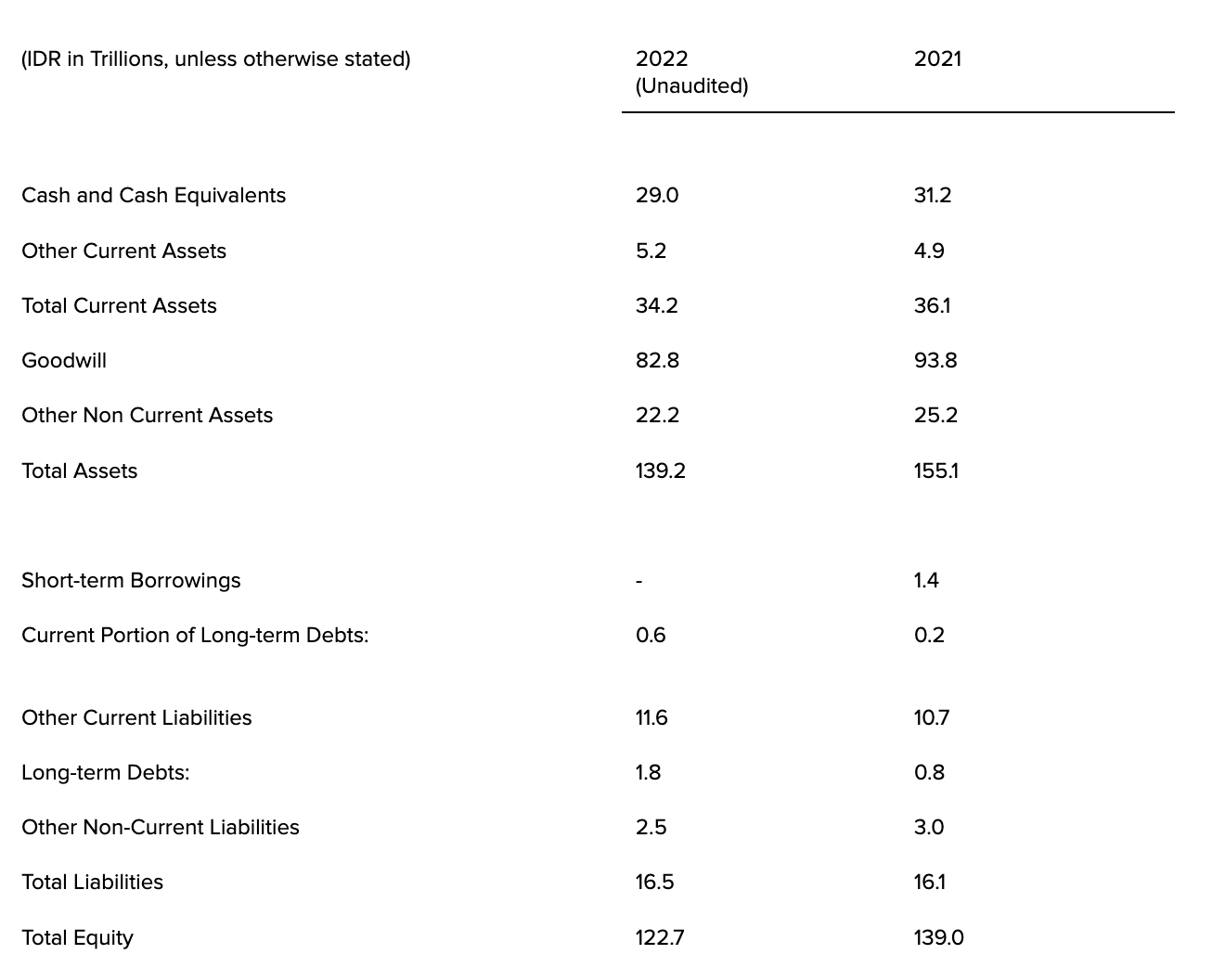

The Group had Rp 29 trillion of cash on hand as of the end of 4Q22, plus a credit facility of approximately Rp 4.65 trillion, of which Rp 1.5 trillion has been utilized. GoTo’s cash position and balance sheet are therefore solid and sufficient to reach positive operating cash flow without any additional external funding.

Group Operational Highlights

The Group remains well on track to reach positive adjusted EBITDA1 by 4Q23, with an expected 60-65% reduction in annual cash burn in 2023. 4Q22 Group Adjusted EBITDA1 was Rp -3.1 trillion, or -1.9% of GTV4, which improved by 52% YoY and 15% QoQ.

Cost saving measures carried out in 4Q22 have resulted in an approximately 20% reduction in average monthly fixed opex costs during the first two months of 2023*, compared with 4Q22, translating to around Rp 200 billion in monthly cost reduction. Incentives and product marketing spend was reduced by 34% YoY in 4Q22, translating to a Rp 2.8 trillion cost reduction.

Despite this, the Group maintained positive growth as a result of its focus on sustainably growing and engaging its high quality consumer base with a pipeline of strategic products, as average consumer spending grew by 24% YoY, reaching a record high of Rp 9.6 million per consumer per year in Q4.

During 4Q22, the number of profitable consumers in On-demand and E-commerce increased by 19% YoY, and contributed to more than 60% of the total GTV4. As incentives were reduced, profitable consumers transacted more and became more profitable, with Q4 Contribution Margin2 per user improving by more than 50% YoY.

These actions contributed to an improvement in take rates of 234 bps and 32 bps YoY for On- demand Services and E-commerce, respectively.

Net Loss stands at approximately Rp 19.5 trillion for the quarter, and Rp 40.4 trillion for the year, increasing from Rp 10.2 trillion in 4Q21 and Rp 25.9 trillion in FY 2021 (on a proforma basis). This was due to several items, which were either non cash or one-off in nature, and do not reflect the Group’s operational performance. The items included a goodwill impairment of Rp 11 trillion associated with the business combination of Gojek and Tokopedia, impairment on investment in JD, as well as an increase in share-based compensation expenses due to an adjustment of the assumed employee turnover rate to reflect the latest historical trend, and one-off restructuring costs. Excluding these items, Net Loss for 4Q22 was approximately Rp 6.5 trillion, an improvement of 36% YoY and 3% QoQ.

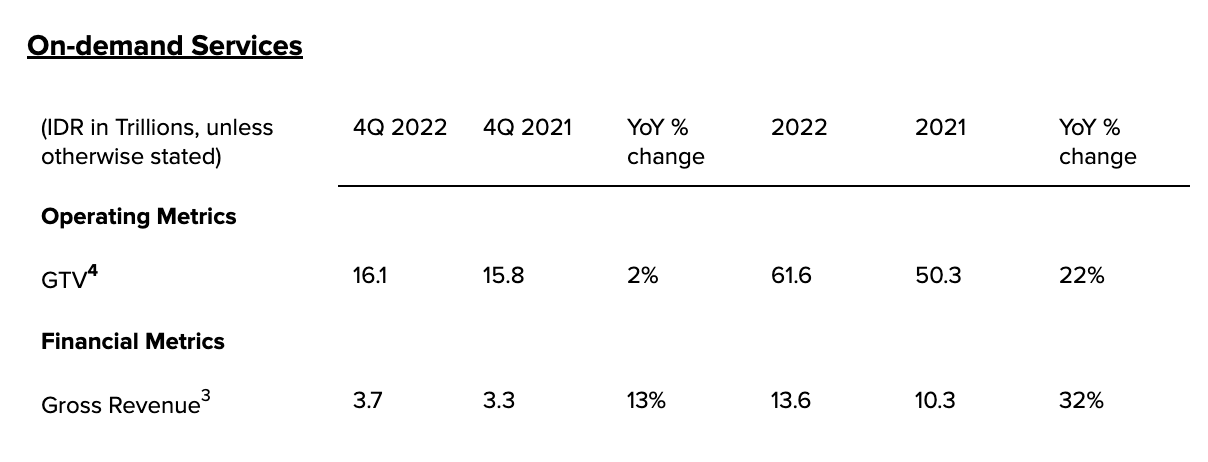

On-demand Services benefitted from continued improvement in mobility services as transport fully recovered to pre-pandemic levels and showed healthy growth despite increases in fuel prices and higher tariffs. This was partially offset by a normalization in Food deliveries due to economic reopening, bringing about more offline consumer spending. We expect this normalization trend to continue in Food orders over the coming quarters.

- Incentives and product marketing expenses for On-demand Services were rationalized by 38% YoY in the fourth quarter with a pivot to high-quality consumers. High-quality consumers increased spending on the platform during the period in spite of the reduced incentives.

- Improved dynamic pricing and mapping technology that boosts efficiency and earnings for driver-partners, helped bring higher service fees during peak hours, particularly in Food delivery. As a result, 4Q22 take rate improved by 234 bps YoY and 94 bps QoQ to 23.1% of GTV4.

- The combined monetization improvements and decreased costs drove Contribution Margin2 for On-demand Services to turn positive in 4Q22, reaching Rp 210 billion, or 1.3% of GTV4, up by 182 bps QoQ.

- Looking ahead, the upward trend is expected to continue into 1Q23 despite macro headwinds. To leverage this momentum, the Group will continue to scale its foundational products that deliver more value and convenience to customers.

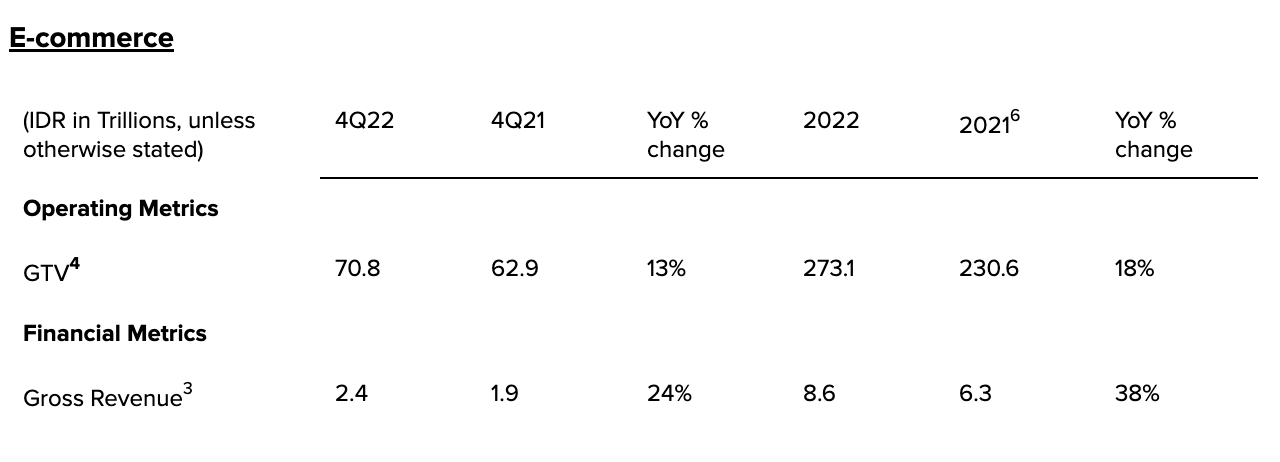

In the E-commerce segment, Tokopedia’s “everything store” approach is working well to capture behavioral shifts toward increased discretionary spending. The year-end and Christmas period helped to drive sales in several categories for the quarter including the food and beverage as well as home and living categories, which benefited from the hosting of festive events at home.

- Driven by improved monetization from value-added merchant app capabilities and improved sales performance of advertising offerings, take-rate grew to 3.4% of GTV4 in 4Q22.

- E-commerce Contribution Margin2 improved in 4Q22, up by 39 bps QoQ to -0.7% of GTV4.

- Looking ahead, the focus in E-commerce will be on improving the availability of intra-city selection for consumers, particularly outside Greater Jakarta, and leveraging the Group’s unique ecosystem to create an aggregated supply chain model, supported by fulfillment centers and an on-demand driver fleet to reduce delivery times and costs.

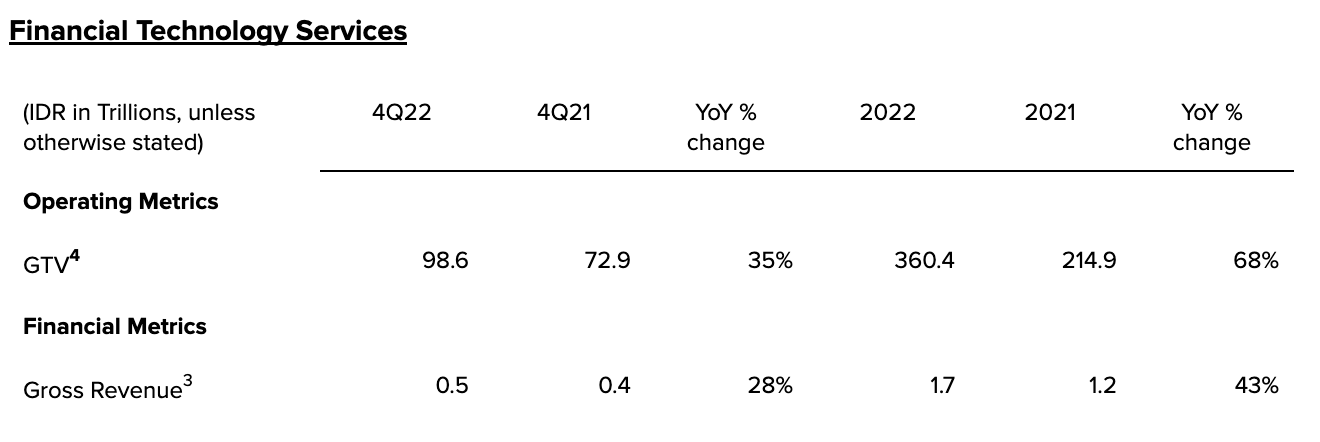

In the financial technology business, payments GTV4 continued its strong growth in 4Q22 despite a reduction in consumer payment incentives of approximately 40% YoY. The lending business also showed good initial traction, with the loan book increasing 40% QoQ. Notably, by the end of 4Q22, the average loan disbursed from PayLater products was profitable, underscoring the Company’s prudent approach.

- GoPay user quality continued to improve, with average spend per GoPay user increasing by 32% for the quarter, compared with 4Q21. This is despite significantly lower incentives per user. Contribution Margin2 therefore improved by 10 basis points QoQ or 31 basis points YoY to -0.2% of GTV4 in 4Q22.

- Gross revenue3 for Fintech increased 28% YoY to Rp 470 billion in 4Q22 on a take rate that remained stable YoY and QoQ. Take rates are expected to increase as the lending business continues to grow.

- GoTo Financial’s merchant businesses, critical components of its offering, have been consolidated into a leaner and more cost-efficient setup to deliver a more cohesive experience to merchants.

- Looking ahead, consumer lending is expected to be a core engine to drive monetization for the Fintech business. GoTo Financial will continue to scale its loan book origination in 2023 while expanding its lending offerings.

Environmental, Social and Governance (ESG)

GoTo continues to invest in the operational shifts required to be consistent with good international industry practice as it relates to ESG performance. Outcomes from the Company’s 4Q22 efforts include:

- Public launch of the Company’s ESG priorities and corresponding roadmaps, with annual targets aligned to and verified by international standards

- Commercial EV pilot with Mitsubishi for GoSend and middle-mile warehouse deliveries

- Heads of Agreement (HoA) partnership with Pertamina New Renewable Energy (NRE) to accelerate the Company’s EV transition goals

- Continued its repurposed packaging program, eliminating excessive packaging and optimizing the accuracy of packaging sizes in Dilayani Tokopedia warehouses (leading to cost savings)

- Pilot Housing Program for driver partners in Solo

- Expanded micro loan and credit pilot programs for driver partners

Company Outlook

As the Group prioritizes high quality users, some slowing of GTV4 is expected over the coming quarters. However, GoTo remains very optimistic on its long term growth opportunities, given its sizable addressable market and continued digital penetration opportunities. The Company continues to invest in and develop foundational products that will enable it to further grow its high quality consumer base in a sustainable way and drive engagement over the long term, while leveraging its unique ecosystem that captures a full range of consumer spending.

GoTo has restructured its fulfillment and 1P e-commerce delivery business and moved it under GoTo Logistics to enable more effective organization. Starting in 1Q23, this will be reported as a separate segment in GoTo’s Financial Statements. The focus for GoTo Logistics will be on reducing the cost-to-serve by moving toward aggregated logistics that mainly serve the E-commerce business.

The Company currently expects:

- To turn Group contribution margin2 positive within the first quarter of 2023

- To achieve positive Group adjusted EBITDA1 within the fourth quarter of 2023

- Full year 2023 Group adjusted EBITDA1 to be between Rp -5.3 to Rp -4.6 trillion.

In line with the Company’s strategy to drive profitability of the businesses and further focus on efficiency, GoTo will not be providing GTV4 and Gross Revenue3 guidance for the full year 2023.

The above outlook is based on current market conditions and reflects the Company’s preliminary estimates, which are all subject to various uncertainties, including those related to cost inflation and the COVID-19 pandemic.

Summary consolidated information of financial position

-END-

About GoTo Group

PT GoTo Gojek Tokopedia Tbk (GoTo Group) is the largest digital ecosystem in Indonesia. GoTo’s mission is to “empower progress” by offering technology infrastructure and solutions that help everyone to access and thrive in the digital economy. The GoTo ecosystem consists of On-demand Services (mobility, food delivery, and logistics), E-commerce (third party marketplaces + official stores, instant commerce, interactive commerce, and rural commerce), and Financial Technology (payments, financial services, and technology solutions for merchants) through the Gojek, Tokopedia, and GoTo Financial platforms.

Indicative figures and Unaudited Consolidated Financial Information

Information presented has been prepared solely as indicative results based on unaudited consolidated selected financial information as of and for the year ended December 31, 2022 of the GoTo Group. In addition, GoTo Group furnished the result for the three months ended and year ended December 31, 2022 with the information December 31, 2021 disclosed as comparative in this document. This information is extracted from the consolidated financial statements of the Company as of and for the year ended December 31, 2022 (with consolidated financial information December 31, 2021 disclosed as comparative) that has been prepared by the Management in accordance with the Indonesian Financial Accounting Standards. The information pertaining to the result and position as of and for the year ended December 31, 2022 and the consolidated financial information for the three months ended December 31, 2022 and 2021 that are in this document has not been audited, reviewed, examined, or applied any procedures. Accordingly, there are no opinions or any other form of assurance expressed with respect to the periods mentioned above.

Currently, the consolidated financial statements as of and for the year ended December 31, 2022 is still in the process of audit finalization.

Forward-Looking Statements

This document may contain forward-looking information or forward-looking statements (collectively, “forward-looking information”). All information contained in this communication that is not clearly historical in nature or that necessarily depends on future or subsequent events is forward-looking information prepared as of the date hereof and is based upon the opinions and estimates of management and the information available to management as of the date hereof. In some cases, forward-looking information can be identified by the use of forward-looking terminology such as "expect", "likely", "may", "will", "should", "intend", "anticipate", "potential", "proposed", "estimate" and other similar words, expressions and phrases, including negative and grammatical variations thereof, or statements that certain events or conditions "may,” or "will" happen, or by discussion of strategy.

Forward-looking information is based upon a number of current internal expectations, estimates, projections, assumptions and beliefs that, while considered reasonable by management, are inherently subject to significant business, economic, competitive and other uncertainties and contingencies. Forward-looking information is not a guarantee of future performance and involves known and unknown risks, uncertainties and other factors (including the risks and uncertainties in the Company’s consolidated financial statements and Management Discussion & Analysis available on the Company’s website), that may cause actual results, performance or achievements to be materially different from the future results, performance or achievements expressed or implied by such forward-looking information. Any estimates, investment strategies or views expressed in this document are based upon current market conditions, and/or data and information provided by unaffiliated third parties, and are subject to change without notice. To the extent any information in this document was obtained from third party sources, the Company has not independently verified that information, and there is a risk that the assumptions made and conclusions drawn by the Company based on such information are not accurate. Except as required by law, the Company disclaims any obligation to update or revise any forward-looking information, whether as a result of new information, events or otherwise. Readers are cautioned not to put undue reliance on this forward-looking information.

Non-IFAS Financial Measures

GoTo Group uses the following non-Indonesian Financial Accounting Standards (IFAS) financial measures including gross revenues3, contribution margin2 and adjusted EBITDA1, to understand and evaluate GoTo Group’s core operating performance. However, the definitions of GoTo Group’s non-IFAS financial measures may be different from those used by other companies, and therefore, may not be comparable. Furthermore, these non-IFAS financial measures have certain limitations in that they do not include the impact of certain expenses that are reflected in GoTo Group’s consolidated financial information that are necessary to run GoTo Group’s business. Thus, these non-IFAS financial measures should be considered in addition to, not as substitutes for, or in isolation from, measures prepared in accordance with IFAS.

These non-IFAS measurements are not intended to replace the presentation of GoTo Group’s financial results in accordance with IFAS. Rather, GoTo Group believes that the presentation of Adjusted EBITDA1 provides additional information to investors to facilitate the comparison of past and present results, excluding those items that GoTo Group does not believe are indicative of GoTo Group’s ongoing operations due to their size and/ or nature. In addition, GoTo Group also presented the Contribution Margin2 that may provide additional information to investors in relation to the results excluding the non-variable expenses and other income/ expenses. Contribution margin2 and adjusted EBITDA1 presented herein may not be comparable to similarly entitled measures presented by other companies, who may use and define this measure differently. Accordingly, you should not compare this non-IFAS measure to those presented by other companies.

Pro Forma Financial Information

GoTo Group furnished the pro forma consolidated information of profit or loss and other comprehensive income as if Tokopedia had been consolidated by GoTo for all the periods presented in this document. The pro forma consolidated information of profit or loss and other comprehensive income have been prepared based on the Company’s combined historical financial information, excluding the amount of historical financial information recognised as intercompany elimination item. Pro forma consolidated information of profit or loss and other comprehensive income is not intended to be a complete presentation of the GoTo Group’s financial performance or results of operations had the transactions been concluded as of and for the periods indicated. In addition, these pro forma information are provided for illustrative and informational purposes only and are not necessarily indicative of the GoTo Group’s future results of operations or financial condition as an independent, publicly traded company.

The pro forma financial information included in this document has been prepared by and is the responsibility of management. This pro forma information has not been audited, reviewed, examined, or applied any procedures with respect to the pro forma financial information, included in this document . Accordingly, there are no opinions or any other form of assurance expressed with respect to any and all pro forma financial information presented in this document.

The pro forma financial information included in this document (i) is presented based on currently available information and estimates and assumptions that the GoTo Group’s management believes are reasonable as of the issuance date of this document; (ii) is intended for informational purposes only; and (iii) does not reflect all decisions that are undertaken by the GoTo Group after the acquisition.

While the pro forma financial information is helpful in illustrating the financial characteristics of the consolidated companies, it is not intended to illustrate how the consolidated companies would have actually performed if the acquisition of Tokopedia in fact occurred on the date of acquisition or to project the results of operations or financial position for any future date or period.

Operating Metrics

LTM ATU5 or Last Twelve Months Annual Transacting Users means the number of unique transacting users in the trailing twelve months. GTV or Gross Transaction Value means gross transaction value, an operating measure representing the sum of (i) the value of on-demand services transactions; (ii) the value of e-commerce transactions for product and services; and (iii) the total payments volume processed through our financial technology services, excluding any inter-company transactions.

1 GoTo Group calculates the adjusted EBITDA, a non-IFAS financial measure, beginning with loss before income tax and adjusting for (i) depreciation and amortization expenses; (ii) finance income; (iii) interest expenses; (iv) loss on impairment of assets of disposal group classified as held for sale; (v) (reversal)/loss on impairment of investment in associates; (vi) loss on impairment of goodwill; (vii) fair value adjustment of financial instruments; (viii) loss on impairment of intangible and fixed assets; (ix) share-based compensation cost (including for the Gotong Royong Program); (x) unrealized foreign exchange (gain)/loss from cash remeasurement; (xi) share of net losses in associates and joint ventures; (xii) (gain)/loss on divestment and dilution of investment in associates and joint ventures, net (xiii) dividend income; and (xiv) non-recurring items.

2 GoTo Group calculates the calculates contribution margin, a non-IFAS measure, beginning with net revenues and deducting total cost of revenues, a portion of sales and marketing expenses relating to the promotional excess and product marketing and others consists of mainly withholding taxes related to sales and marketing expense and other insignificant expenses.

3 Gross revenue represents the total Rupiah value attributable to GoTo Group from each transaction, without any adjustments for incentives paid to driver-partners and merchant partners or promotions to end-users, over the period of measurement. For a reconciliation of net revenue to gross revenue, please refer to the section “Non-IFAS Financial Reconciliation.”

4 GTV means gross transaction value, an operating measure representing.

a. the sum of the time value of the transactions from On-demand Services.

b. the sum of the value of the product and services recorded on our E-commerce Segment.

c. the sum of the total payments volume, or TPV processed through our platform of Financial Technology Services.

d. and excluding amounts from inter-Company transactions between entities within the Company that are eliminated upon consolidation.

5 LTM ATU means trailing twelve months of unique transacting users.

6 Comparisons are made against the pro forma financial and operating metrics for the twelve months ended December 31, 2021, which were derived from the unaudited consolidated historical financial information of GoTo Group and Tokopedia, and certain adjustments and assumptions have been made regarding our Group after giving effect to the acquisition of Tokopedia. Such numbers are presented for illustrative purposes only and may not be an indication of what the Company’s financial position or results of operations would have been or for any future periods.

Contacts:

Media

GoTo Group: corporate.affairs@gotocompany.com

Investors/analysts

GoTo Group: ir@gotocompany.com

The Piacente Group: goto@thepiacentegroup.com